UP Board Solutions for Class 10 Commerce Chapter 1 Final Accounts

UP Board Solutions for Class 10 Commerce Chapter 1 Final Accounts

Final Accounts Objective Type Questions (1 Mark)

Question 1.

……… is not a fixed asset. (UP 2014)

(a) Land and Building

(b) Stock

(c) Furniture and Fixtures

(d) Plant and Machinery.

Answer:

(b) Stock

Question 2.

…………. is shown in Trading Account. (UP 2014)

(a) Gas and Fuel

(b) Salary

(c) Commission

(d) Rent.

Answer:

(a) Gas and Fuel

Question 3.

Profit and Loss Account is prepared by: (UP 2014)

(a) Partnership Firm

(b) Sole Trader

(c) Company

(d) All of these.

Answer:

(d) All of these.

Question 4.

……….. is not current liability. (UP 2013)

(a) Creditors

(b) Bills Payable

(c) Bank Overdraft

(d) Capital.

Answer:

(d) Capital.

Question 5.

……….. is current Asset. (UP 2012, 16)

(a) Cash

(b) Furniture

(c) Machinery

(d) None of these.

Answer:

(a) Cash

Question 6.

Net Profit is shown in the capital by: (UP 2012)

(a) Adding

(b) Deducting

(c) Adding or Deducting

(d) All of these are correct.

Answer:

(a) Adding

Question 7.

………. is not shown in Trading Account. (UP 2013, 16)

(a) Carriage inward

(b) Carriage outward

(c) Wages

(d) Factory Light

Answer:

(b) Carriage outward

Question 8.

………. is not an account: (UP 2015)

(a) Trading Account

(b) Profit and Loss Account

(c) Balance Sheet

(d) All of these.

Answer:

(d) All of these.

Question 9.

………… is shown in the balance sheet: (UP 2015, 17)

(a) Salary

(b) Rent and Tax

(c) Repairs

(d) Cash.

Answer:

(d) Cash.

Question 10.

Trade expenses are written in: (UP 2015, 18)

(a) Trading Account

(c) Balance Sheet

(b) Profit and Loss Account

(d) None of these.

Answer:

(c) Balance Sheet

Question 11.

Which of the following is Fixed Asset Account? (UP 2019)

(a) Capital

(b) Bills payable

(c) Debtors

(d) Plant and Machinery.

Answer:

(d) Plant and Machinery.

Final Accounts Definite Answer Type Questions (1 Mark)

Question 1.

What kind of Assets have no real value?

Answer:

Fictitious.

Question 2.

What kind of Assets come into existence on the happening of certain event?

Answer:

Contingent.

Question 3.

What term is used for the process or manner of disclosing Assets and Liabilities in Balance Sheet?

Answer:

Marshalling.

Question 4.

Write the name of the book in which miscellanceous expenses are recorded. (UP 2014, 18)

Answer:

Petty Cash Book.

Question 5.

What kind of expenditure is done for the acquisition of Assets with a view to increase productivity?

Answer:

Capital.

Final Accounts Very Short Answer Type Questions (2 Marks)

Question 1.

What is meant by Gross Profit?

Answer:

Gross Profit: The excess of the selling price of the sold goods over their purchase price including all direct expenses is called Gross Profit.

Question 2.

What are Current Assets?

Answer:

Current Assets: Current Assets are assets which are required by the business for the purpose of resale, as stock in trade or such assets which are constantly circulating and arise out of usual business dealings.

Question 3.

What is meant by Fixed Assets? Mention any two. (UP 2013)

Answer:

Fixed Assets: Fixed assets are those assets which are held by way of possession and not for purpose of resale. They are permanent in nature and the business is carried on with their help.

Example: Land, Building etc.

Question 4.

Where would you show adjustment relating to Accrued Income? (UP 2019)

Answer:

Assets side of Balance sheet and credit side of P & L a/c.

Question 5.

Which account is prepared for knowing the net profit? (UP 2019)

Answer:

Profit and Loss Account.

Final Accounts Short Answer Type Questions (4 Marks)

Question 1.

What do you understand by Final Account? (UP 2014, 16)

Answer:

Final Account is the final process of accounting. The final account is prepared to show the final result of the company in a specific period. Trading, Profit and Loss account and Balance Sheet are included in the final account.

Question 2.

Write the characteristics of fixed assets. (UP 2014)

Answer:

- Fixed assets are held by way of possession and not for the purpose of resale.

- Fixed assets are permanent in nature and the business is carried on with their help.

Question 3.

Give differences between Trial Balance and Balance Sheet.

Answer:

Difference Between Trial Balance and Balance Sheet.

| Trial Balance | Balance Sheet |

| 1. Trial Balance Check only arithmetical accuracy of accounts. | 1. Balance Sheet is prepared to find out the financial position of the business. |

| 2. Trial Balance is prepared before the preparation of Final Accounts. | 2. Balance Sheet is the last content of the Final Accounts. |

| 3. It is not compulsory to prepare the Trial Balance. | 3. It is compulsory to prepare the Balance Sheet. |

Final Accounts Long Answer Type Questions (8 Marks)

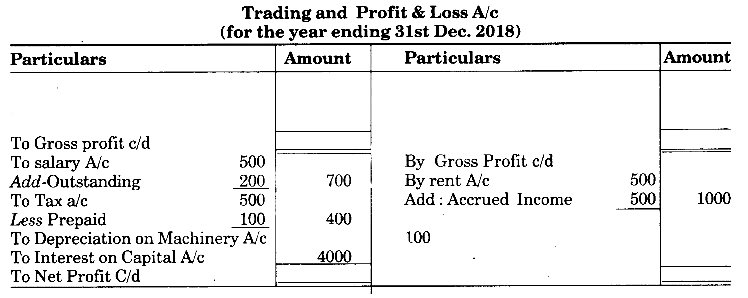

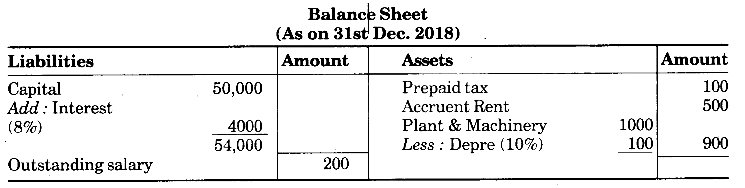

Question 1.

Keeping in mind adjustments for outstanding salary prepaid tax, accrued income, interest on capital @ 8% and 10% depreciation on plant and furniture, prepare Trading and Profit & Loss Account and Balance Sheet of Sagar Brothers with imaginary figures:

Answer:

Question 2.

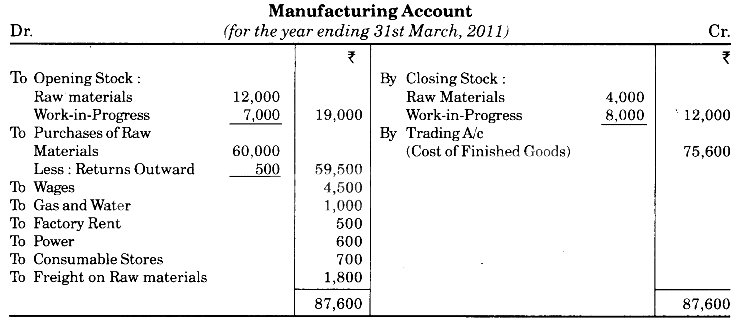

What is the manufacturing account? How does it differ from a Trading Account? Give an example of a manufacturing account using imaginary figures. (UP 2004)

Answer:

Manufacturing Account: Manufacturing Account is prepared by those undertakings, which undertake or engaged in the production activities. Manufacturing Account is prepared for knowing the cost of goods produced by the concern which further helps in fixing the selling price of the goods produced. A manufacturer purchases the raw materials for selling them by transforming them into finished goods. For this, several expenses are to be incurred by him like fuel, power, electricity, water, coal etc.

Fuel and Power: When fuel and power are used for undertaking the production or running the machinery, they are debited to Manufacturing or Trading Account as the case may be. The light used for lighting purpose does not mean power. Power should not be understood as lighting which is discussed below:

Lighting: The electricity which is used for making the Lighting in the factory building is shown at the debit side or Manufacturing or Trading Account. If the same meter of electricity is used for Lighting the factory and office building then the expenses shoukPbe apportioned appropriately. The expenses of Lighting for office building should be charged to Profit and Loss Account.

Stock: Stock of raw materials, semi-finished goods and finished goods are the three kinds of opening or closing stock remaining with the manufacturer.

The manufacturer or producer can prepare his Trading Account in three ways:

- To prepare Manufacturing and Trading Account separately in such a way as to transfer the balance of Manufacturing Account to Trading Account.

- All types of stock, purchases sales and direct expenses are to be recorded in one account, known as Trading Account.

- After putting down the heading of Trading Account, its upper portion is prepared as Manufacturing Account and lower portion as Trading Account.

Example.of a Manufacturing Account:

Question 3.

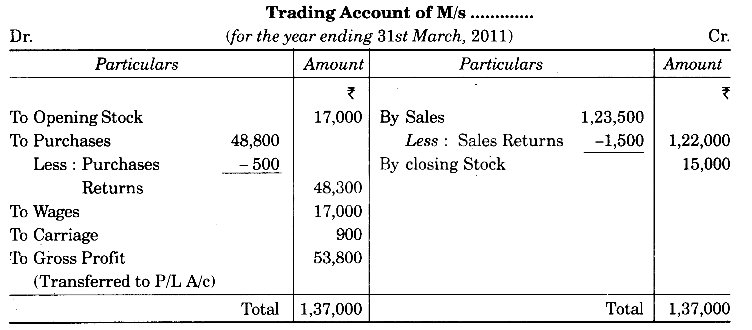

What are the objects of preparing Trading Account? How does it differ from Profit and Loss Account? Prepare Trading Account using imaginary figures. (UP 2004)

Or

What is a Trading Account? Distinguish between the Trading Account and Profit and Loss Account. Give a specimen of Trading Account. (UP 2008)

Answer:

Trading Account: The Trading Account is an account which shows the result of the buying and selling of goods. It contains in a summarized form of all the transactions occurred during a trading period which has a direct relation to the goods dealt in by the business. Trading Account is a part of the Profit and Loss Account and is made at the end of the financial year.

Gross Profit and Gross Loss: The excess of the selling price of the sold goods over their purchase price including all direct expenses is called Gross Profit. If the cost of the purchase price including all direct expenses exceeds the selling price of the goods sold, it is called Gross Loss. Gross Profit is transferred to the credit side and Gross Loss is transferred to the debit side of Profit and Loss Account.

To Know the Cost of Goods Sold: To know the Gross Profit or Gross Loss the calculation of the actual cost of goods sold is very necessary.

The total of the following gives the cost of goods:

- Purchase price of the goods after deducting purchase returns.

- Carriage paid on purchases like Railway Freight, Carriage etc. These expenses are termed as Carriage Inward.

- Payment of toll tax or any other taxes in bringing the goods.

- Expenses for clearing charges made for goods.

- Wages in connection with goods.

- Manufacturing expenses, like fuel, power, coal etc.

The amount of Sales return is deducted from the number of Sales and then the value of a Closing stock is added to it. From the figure so obtained the total of above expenses including opening stock is deducted and the balance amount is the Gross Profit.

Difference between the Trading Account and Profit and Loss Account:

Following are the points of difference between Trading and Profit and Loss Account:

| Trading Account | Profit and Loss Account |

| 1. Trading Account is prepared for ascertaining the Gross Profit. | 1. Profit and Loss Account is prepared for ascertaining the Net Profit. |

| 2. Direct expenses are transferred to Trading Account. | 2. Indirect expenses are transferred to Profit and Loss Account. |

| 3. The balance i.e., Gross Profit or Loss is transferred to Profit and Loss Account. | 3. The balance i.e., Net Profit or Loss is transferred to Capital Account or Balance Sheet. |

| 4. Trading Account is prepared before the Profit and Loss Account. | 4. Profit and Loss Account is prepared after the Trading Account. |

| 5. Trading Account is a part of the Profit and Loss Account. | 5. Profit and Loss Account is a principal Account. |

Specimen of Trading Account:

Question 4.

Why is the Balance Sheet prepared? What is the difference between the Trial Balance and the Balance Sheet? (UP 2002, 16)

Or

What do you understand by Balance Sheet? (UP 2015, 17)

Answer:

The information revealed by the Trading and Profit and Loss Account is no doubt very useful to the owner of a business, as it enables him to know the Gross and Net Profit or Loss. The Assets and Liabilities of a business change from day to day, as a result of business transactions. He also wants to find out the correct financial position of his business until the end of each financial period. In the first place, he would like to know whether net profit or loss disclosed by the Profit and Loss Account is correct and if so, then whether the impact of the same has been correctly shown in the Capital Account or not. The businessman is always concerned about his true position of Assets and Liabilities. In order, therefore, to obtain this information at the end of the trading period, he has to set out his Assets and Liabilities as on that date in the shape of a statement and this statement is called the Balance Sheet.

Definition of Balance Sheet:

A Balance Sheet may be defined as a statement prepared with a view to determining the exact financial position of a business on a certain fixed date.

The Balance Sheet is prepared from the Trial Balance after all the balances of Nominal Account are transferred to the Trading, Profit and Loss Account and the corresponding accounts in the ledger are closed. The balances now left in the Trial Balance and accounts remaining open in the ledger represent either Personal Accounts or Real Accounts. In other words, they represent either Assets or Liabilities existing at the date of the financial closing.

All such Assets and Liabilities are shown in the Balance Sheet in a classified form. On the right-hand side are shown the various Assets or possessions of the business, and on the left-hand side, the various Liabilities, i.e., the amount which the business owes to others. The excess of Assets over Liabilities represent the Capital. The figure of the capital should tally with the balance of the Capital Account in the ledger after adjustment of the Profit and Loss in the Capital Account.

Difference between the Trial Balance and the Balance Sheet:

| Trial Balance | Balance Sheet |

| 1. Trial Balance tests the arithmetical accuracy of accounts. | 1. Balance Sheet is prepared to find out the financial position of the business. |

| 2. Trial Balance includes the Personal, Real and the Nominal accounts. | 2. Balance Sheet contains only Personal and Real accounts. |

| 3. The Balances of the accounts in the Trial Balance are shown in the same order as they appear in the ledger book. | 3. The Balances in the Balance Sheet are shown either in order of liquidity or in order of permanence. |

| 4. Trial Balance is prepared before the preparation of final accounts. | 4. Balance Sheet is the last content of the final accounts. |

| 5. Closing stock is not included in the Trial Balance. | 5. It is necessary to show the closing stock in the Balance Sheet. |

| 6. The terms ‘Dr.’ and ‘Cr.’ are used in the Trial Balance. | 6. The terms used in the Balance Sheet are ‘Assets’ and ‘Liabilities’. |

| 7. It is not compulsory to prepare the Trial Balance. | 7. It is compulsory to prepare the Balance Sheet. |

Specimen of Balance Sheet:

Balance Sheet. (as on …..)

| Particulars | Amount (₹) | Particulars | Amount (₹) |

| Bank Overdraft Bills Payable Loan Sundry Creditors Capital Add: Net Profit ………. ……….. Less: Drawings ………………. ……………… |

……….. ………. ………. ……….. ……….. ……..……….. |

Cash in Hand Cash at Bank Investments Bills Receivable Sundry Debtors Closing Stock Furniture Machinery and Plant Land and Building Motor Car Tools Goodwill |

……….. ……….. ………. ………. ……….. …………. ……….. ………. ………. ………. ……… ………. |

Question 5.

What do you mean by Balance Sheet? State classification of assets and liabilities. (UP 2002, 16)

Answer:

Manufacturing Account: Manufacturing Account is prepared by those undertakings, which undertake or engaged in the production activities. Manufacturing Account is prepared for knowing the cost of goods produced by the concern which further helps in fixing the selling price of the goods produced. A manufacturer purchases the raw materials for selling them by transforming them into finished goods. For this, several expenses are to be incurred by him like fuel, power, electricity, water, coal etc.

Classification of Assets and Liabilities:

1. Fixed Assets: Fixed Assets are those assets which are held by way of possession and not for the purpose of resale. They are permanent in nature and it is by their help that the business is carried on.

Example: Land, Building, Plant Machinery, Tools, Furniture, Fittings, etc.

2. Floating Assets: Floating assets are assets which are required by the business for the purpose of resales, such as stock in trade or such assets which are constantly circulating and arise out of usual business dealings. They are held temporarily for subsequent conversion into money.

Example: Debtors, Stock, etc.

3. Wasting Assets: The assets which lose their value in a diminishing manner are known as Wasting Assets.

Example: Patent of land, Copyright, etc.

4. Liquid Assets: Liquid Assets are assets which can be immediately converted into cash.

Example: Bills Receivable, Cash at Bank, etc.

5. Nominal Assets: Nominal Assets are imaginary assets which do not have any shape or volume. They are also called Fictitious Assets.

Example: Goodwill, Prepaid Expenses, Accrued Income.

Classification of Liabilities:

1. Fixed Liabilities: Liabilities which are not to be paid in the near future but are payable after a long period is known as Fixed Liabilities. There are some liabilities which are paid after the liquidation of a business.

Example: Capital, long term loan, etc.

2. Current Liabilities: Liabilities which are to be paid in the near future are known as Current Liabilities.

Example: Creditors, Bank Overdraft, Bank Loan, Bills Payable, etc.

3. Contingent Liabilities: Contingent Liabilities are those liabilities which are paid on happening or non-happening of some event.

Example: Suppose there is a matter under consideration in a court of law regarding less payment of taxes. If the decision of the court is favourable then no payment will be made and if the decision is unfavourable then the amount decided by the court will have to be paid.

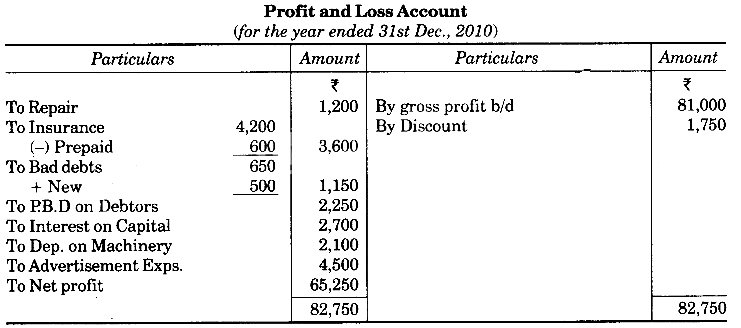

Question 6.

Prepare Profit and Loss Account of M/s Keshav and Sons, for the year ending on 31st December 2010.

From the following information:

Cash in Hand Rs. 1,000; Cash at Bank Rs. 5,000; Machinery Rs. 21,000; Debtors Rs. 45,000 ; Discount (Cr.) Rs. 1,750 ; Repairs Rs. 1,200 ; Bad Debts Rs. 650 ; Advertising expenses Rs. 4,500; Insurance Premium Rs. 4,200; Capital Rs. 45,000; Gross Profit Rs. 81,000.

Adjustments:

(i) Prepaid Insurance Premium Rs. 600.

(ii) Bad debts Rs. 500 and reserve for doubtful debt @ 5% on debtors

(iii) Interest on Capital @ 6% p.a.

(iv) Depreciation on Machinery @ 10%. (UP 2018)

Answer:

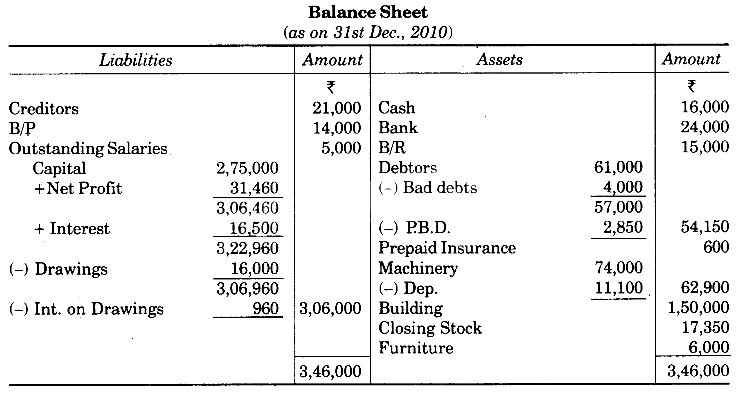

Question 7.

Prepare Balance Sheet of M/s Kingsley Brothers as on 31st December, 2010 from the following information: (UP 2011)

Cash Rs. 16,000; Bank Rs. 24,000; Debtors Rs. 61,000; Machinery Rs. 74,000; Building Rs. 1,50,000; Bills Receivable Rs. 15,000; Bills Payable Rs. 14,000; Creditors Rs. 21,000; Capital Rs. 2,75,000 ; Drawings Rs. 16,000 ; Bad Debt Reserve Rs. 4,500; Closing Stock Rs. 17,350; Net Profit Rs. 31,460; Furniture Rs. 6,000.

Other Information:

Net Profit was calculated after the following adjustments:

(i) Outstanding salaries Rs. 5,000.

(ii) Prepaid insurance premium Rs. 60.

(iii) Bad Debts Rs. 4,000 and reserve for Bad Debts @ 5% on debtors.

(iv) Interest on Capital and Drawings @ 6%.

(v) Depreciation on Machinery @ 15%. (UP 2011)

Answer: